You have just returned from your honeymoon, you have unpacked the gifts, and you are ready to start your life as a married couple. You head into your local bank branch, marriage certificate in hand, ready to update your surname on your debit card and bank statements.

But instead of a simple "congratulations," you are met with a refusal. The bank teller tells you that your marriage certificate isn't enough evidence to change your name to the one you want.

If this sounds familiar, do not panic. This is one of the most common complaints we hear from newlyweds. While government bodies like the Passport Office are generally quite flexible, UK banks operate under strict financial regulations and risk policies.

Here is why your bank might be saying "no" and exactly what you can do to fix it.

The Core Problem: Anti-Money Laundering (AML)

First, it helps to understand why banks are so difficult. It isn't just to be annoying. Banks are under immense legal pressure to prevent fraud and money laundering. They must be 100% certain of a customer's legal identity.

A Marriage Certificate proves you got married. It does not explicitly state "This person's name is now X." It simply shows the names of the two people who married. By tradition, you are allowed to take your spouse's name, but any deviation from that standard tradition makes bank compliance teams nervous.

Reason 1: You Are Double-Barrelling

This is the number one reason for rejection.

The Scenario: Your surname is Smith. You marry Mr. Jones. You want to become Smith-Jones. You present your marriage certificate which shows both names.

The Rejection: The bank refuses because your marriage certificate does not explicitly say "Smith-Jones." It shows "Smith" and "Jones" separately. While the Passport Office will usually accept this combination without issue, many banks view a double-barrelled name as a new name entirely, rather than just "taking the spouse's name."

The Fix: You need a Deed Poll. A Deed Poll bridges the gap between the two names on the certificate and the hyphenated version you want to use. It gives the bank a concrete legal document that links your old identity to your new, double-barrelled identity.

Reason 2: You Are "Meshing" Names

The Scenario: You (Green) and your partner (Wood) want to become the Greenwoods.

The Rejection: A marriage certificate gives you absolutely no legal right to create a new surname or merge names. If the name you are asking for does not appear in full on the certificate, the bank cannot accept it.

The Fix: This is a mandatory Deed Poll situation. You and your partner must both change your names via Deed Poll to the new "meshed" name before the bank will update your accounts.

Reason 3: Moving a Maiden Name to a Middle Name

The Scenario: You want to take your husband's surname but keep your maiden name as a middle name.

The Rejection: As with double-barrelling, banks see this as a change to your middle name, not just your surname. A marriage certificate only covers surname changes by tradition. It does not authorise changes to forenames or middle names.

The Fix: You must use a Deed Poll to officially add your maiden name as a middle name. The bank will then accept this document without question.

Reason 4: Inconsistent Policies and Staff Training

Sometimes, the computer systems are fine, but the human element fails. Bank staff turnover is high, and specific knowledge about name change conventions can be patchy.

One branch might accept a double-barrelled name with just a marriage certificate, while a branch of the same bank down the road refuses it. Some staff may erroneously believe that if your passport hasn't been changed yet, they can't change your bank account (this is usually false; you can change your bank details before your passport, provided you have the right evidence).

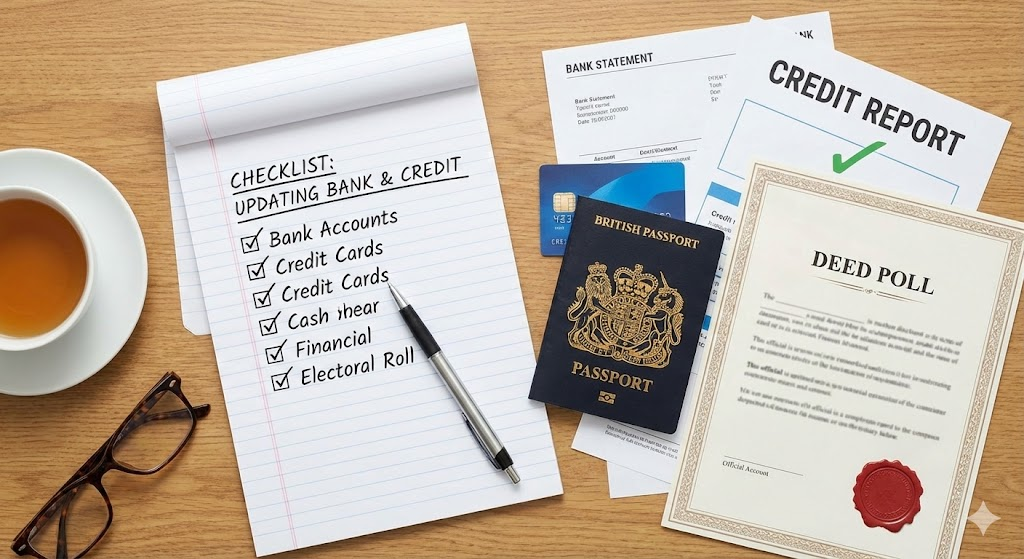

How to Fix the Situation: A Step-by-Step Guide

If you have been turned away, follow these steps to get your account sorted.

Step 1: Verify Your Request

Check what you are asking for. If you are simply taking your partner's exact surname (e.g., changing from Smith to Jones), the bank must accept your marriage certificate. If they refuse this, it is a training error. Ask to speak to a manager or raise a formal complaint.

Step 2: Get a Deed Poll (The "Silver Bullet")

If you are double-barrelling, meshing, or moving names around, do not waste energy arguing with the bank manager. Their compliance team will likely overrule them anyway.

Obtaining a Deed Poll is the fastest, cheapest, and least stressful way to solve this. It provides an indisputable legal chain of evidence. When you present a Deed Poll alongside your marriage certificate, the bank has no grounds to refuse you. It ticks every box for their fraud prevention team.

Step 3: Update Your ID First (Optional but Helpful)

While not always strictly necessary, having your driving licence updated first can help. The DVLA is free to update and usually faster than the Passport Office. Walking into the bank with a Deed Poll and a Driving Licence in your new name makes it very difficult for them to say no.

Step 4: Visit in Person

While some modern banks (Monzo, Starling) allow digital updates, high street banks (Barclays, Lloyds, HSBC, Santander) usually prefer you to visit a branch. Take your original documents (no photocopies). If you have a Deed Poll, take that. If you have updated your passport, take that too.

Summary

It can be incredibly frustrating to feel like your identity is being debated by a bank teller. However, the rule of thumb is simple: If the name you want isn't printed clearly on your marriage certificate, get a Deed Poll.

A Deed Poll removes the ambiguity. It turns a "maybe" into a "yes" and allows you to get back to enjoying your marriage rather than fighting with compliance departments.

Struggling with a stubborn bank? Contact us today to order a Deed Poll. We can have your official documents drafted and sent to you within days, ensuring your bank accepts your new name instantly.

![[Person struggling with online form due to name error]](/media/blog/images/1.jpg)